Buy and Hold means holding an asset through your financial objective’s time horizon. But that does not mean Buy and Forget. Periodically review your overall portfolio and individual holdings. Ensure they remain best in class, meet your needs, and fit within your Investor Profile and Target Asset Allocation. What factors impact portfolio review frequency?

“How does portfolio risk impact review frequency?”

A relatively low risk portfolio may be reviewed less often than one with higher investment risk.

And that reflects both the type of asset and the level of diversification.

A low risk portfolio with one 5-year term deposit needs less a rigorous review than one with a variety of small cap, emerging market equities.

As well, investing in a broad index fund, with many holdings across different sectors and market caps, may manage overall risk better than if you created your own portfolio out of shares in Google, Amazon, Facebook.

“How do general economic and market conditions impact reviews?”

If inflation causes an increase in the prime lending rate, all borrowers will face interest rate hikes. The lower credit rating will be hit hardest, but even high quality borrowers will have to pay higher costs.

If a war breaks out where you live, manage a business, or invest, you will be affected.

The greater the probability that your investments will be impacted by systematic risks, the shorter the time span between reviews. Or, when you see a systematic risk arising, that may trigger a review.

The purpose of creating a well-diversified portfolio helps cope with systematic risk. If Canada experiences bad economic times, that may be buffered by also holding investments in Australia and Germany. If the equity markets go into a bear market, owning some fixed income (at a low to negative correlation coefficient), may provide some portfolio protection.

If your portfolio is not well-diversified, it is more at risk of systematic risk problems.

“Does my personality affect periodicity of reviews?”

Yes.

Some investors are more risk averse than others. Low-risk investors will often prefer a safer investment portfolio. That should mean less review time. However, their personality may be such that they will want quarterly or semi-annual reviews, regardless of the portfolio risk.

Conversely, some investors should be reviewing their portfolios (perhaps) quarterly. But their personality causes them to review every few years, when intending to sell something or the world is on fire.

As well, some people are very detail focused and some are quite relaxed. The detail oriented investor will likely want more frequent reviews (and spreadsheets with adjusted cost base, unrealized gains, yields, and such).

“Anything else that I need to consider?”

Material change.

Material changes are events that cause you to alter your decision-making.

You are single, living the good life. Not a care in the world. How you manage your life is a certain way. Then you get married and what was fine two years ago has now changed. Maybe vacation decisions went from a golf vacation with the gang or a trip to Ibiza to now choosing between the Louvre in Paris versus Tuscan wine tours.

Then, you decide to have a baby. Suddenly, you are googling “life insurance.”

Similar if you lose your job, get a promotion, have an accident, etc. Things that change your outlook and decisions.

With investments, material change is similar.

Much less of an issue with well-diversified portfolios. More an issue with less diversified investments, that are exposed to nonsystematic risks. Risks that are specific to that asset.

For example, you researched junior mining companies and found an excellent company. You invest. But three years later, management starts taking shortcuts in their operations. The company is now being sued for poor reclamation practices and environmental damage. Do you continue holding because – darn it – your strategy is to Buy and Hold? Or do you take that material information and revise your assessment based on real-time knowledge?

If you are not prepared to reassess investments in light of new information, perhaps you still hold shares in Enron, Kodak, Blockbuster, and horse and buggy companies.

But it should be significant information. Otherwise, you end up trading based on market noise and non-material events. It can take some skill and experience to separate out the material from non-material information. And yet another advantage to focusing on well-diversified investment products over individual stocks, bonds, etc. Much less concern in tracking individual assets, as the overall diversified portfolio helps to manage those nonsystematic risks.

In previous episodes, the emphasis was on investing in well-diversified investment products when employing a Buy and Hold strategy. Does Buy and Hold also work with non-diversified assets, such as individual stocks or bonds?

In this context, we are talking mainly about individual stocks and bonds. As well as other assets that may experience nonsystematic risk features and can be bought on an individual basis. A painting, home, stock option.

For example, a fund that invests solely in gold bullion may not be well-diversified. But investors tend to purchase gold as a niche investment to assist in diversifying the overall portfolio. So they are unconcerned about its lack of diversity.

Even broader stock or bond funds may not be well-diversified. Review the number of holdings in total, as well as the overall asset percentage of the top 10 holdings for too much concentration in limited holdings. Geography, capitalization and sector can also impact fund diversification. With bond funds, variables such as effective duration, credit quality, currency, geography, and issuer type can affect overall diversification.

But for these purposes, we will speak primarily about individual stocks and bonds, such as Coca-Cola or Google shares.

“Is it possible to build a well-diversified investment portfolio with individual assets?”

Yes.

However, you probably need a critical mass of investment capital to properly diversification.

Maybe you need 30-50 stocks. Some exposure to Canada. Also, the global markets. Do you want to diversify amongst small, medium, and large cap companies? Or through different industries and sectors? The more portfolio diversification you seek, the more holdings you need. And that requires capital to spread out your wealth.

Then, factor in additional asset classes such as fixed income. The number of portfolio holdings keeps growing.

So, yes, possible. Just takes time, energy, and capital. Much more effective and efficient to simply buy a ready-made fund.

I would note that most people create non-diversified portfolios. They hold 6-10 “fantastic” stocks and are fine in doing so. Perhaps they do well, perhaps not. If they invested in Amazon, Google, Apple, Facebook, Netflix, and Tesla, they will have done wonderfully versus the market.

The issue here is more what happens to the portfolio if Teslas begin to catch fire. Or the US and Australian governments crack down on Facebook. Or the EU hammers Google for its practices. Is there a company being created today that will cause Netflix to become the next Blockbuster? And so on.

That is the purpose of diversification. Spreading out the stock specific risk. And hedging your bets.

“How will my investment costs be impacted under this approach?”

The more investments you own, the greater the investment costs.

Not management fees to a fund company. But transaction fees when you buy and sell holdings. Perhaps tax when you sell and trigger a capital gain. Opportunity cost in spending time to monitor and maintain a portfolio with 30-50 stocks. Then add in bonds and any other asset classes and that is a fair amount of work.

“This will work well if I invest in highest-quality, ‘buy and forget’, holdings, right?”

Yes, you do want to invest in high-quality stocks and bonds.

But what is high-quality? An investment that is quality today, may not be quality tomorrow. And what is quality tomorrow, may not even exist today.

Not too long ago, companies like GM, GE, Kodak, Sears, etc., were household names and popular brands. With excellent stock. Today, they are all gone from their days of fame.

In their place, we now have Google, Tesla, Facebook, Netflix, etc. Companies that have really only been around for the last 20 or so years.

Kodak joined the Dow 30 in 1930 and departed in 2004. Before declaring bankruptcy in 2012.

Will Google, Amazon, Apple, Tesla, Nike, Netflix, and Facebook, all last that long? Or will there be new companies emerge that, as Apple did to Kodak and Netflix did to Blockbuster, knock off these high-quality companies?

Buy and Hold does not mean Buy and Forget. You need to monitor your portfolio and ensure it invests in quality holdings.

Diversified investment funds help achieve this. But when trading individual stocks and bonds, you need to constantly review and adjust your portfolio. This may results in hard costs (transaction fees, tax). It will definitely result in added time and energy to review your portfolio. If you have the free-time, interest, and knowledge, great. But for most investors working jobs in non-investment areas, sacrificing time to study investments becomes onerous.

Why not just stick to a well-diversified, low-cost fund instead?

A legitimate concern when using a Buy and Hold investment strategy is managing market volatility. How do investors use complementary investment strategies and tactics to reduce risk in bear-markets and short-term fluctuations.

“What exactly is a ‘bear’ market? How does it differ from a ‘bull’ market?”

A bear market is a prolonged period of falling prices. Usually, 20% from its previous high.

A bull market is a prolonged period of rising prices. Usually, rising at least 20% from its previous low.

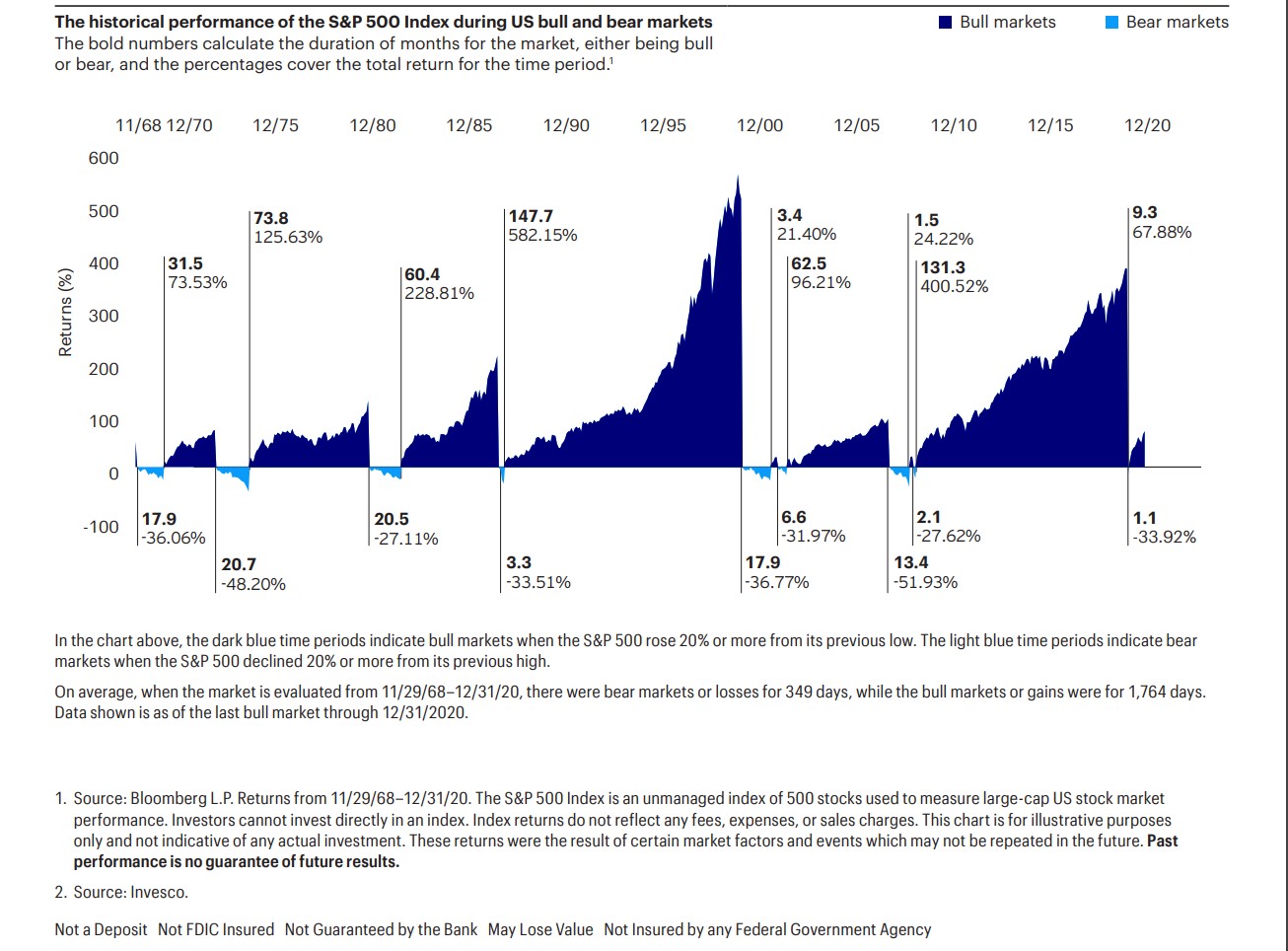

“What is an average time period for bull and bear markets?”

Per Invesco, from 1968 to the end of 2020, the average bull market has averaged 1764 days in length (4.8 years). Once a bull gets underway, it tends to stay for an extended period.

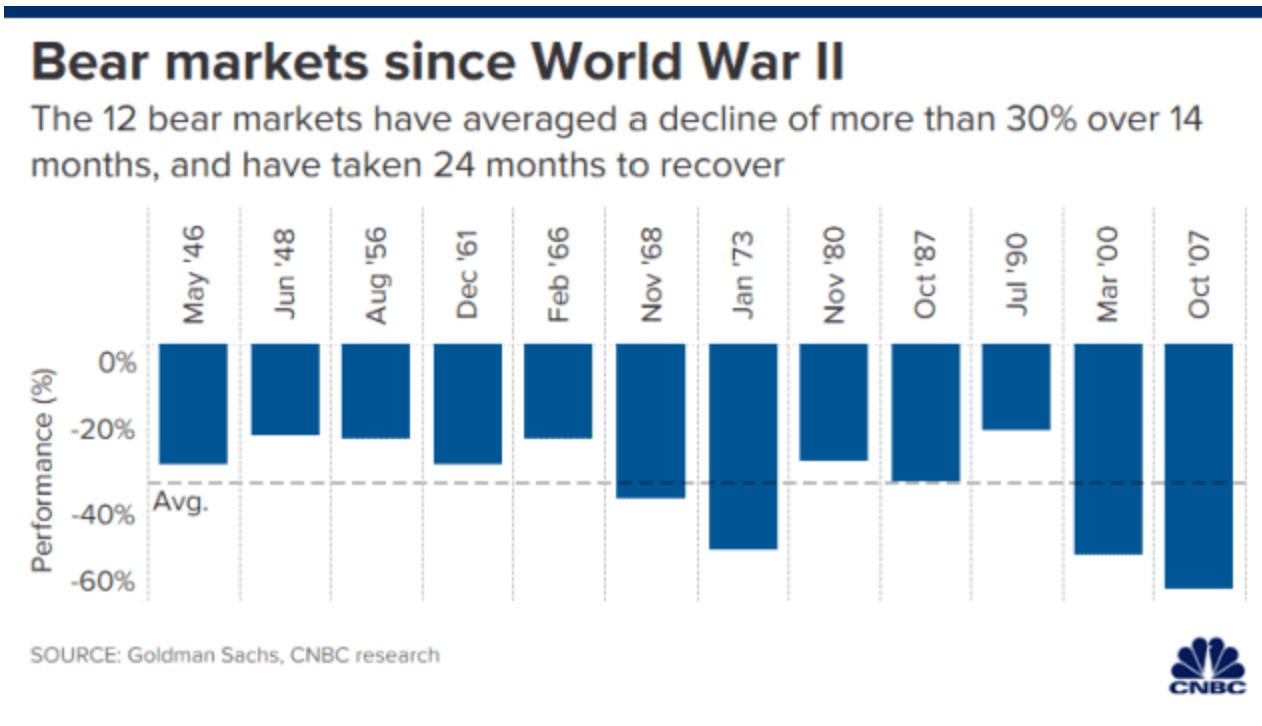

During that same period, there have only been about 7 truly, sustained bear markets that were over 90 days in length. The average length of a bear market has been 349 days. Much shorter in duration than the bull runs.

However, one must factor in the recovery time as well. If you purchased at $100 and it fell to $70, you want to assess how low it took to get back to $100. Not just when the bear market ended and prices began to increase.

Per Goldman Sachs, it has taken the S&P 500 about 24 months to fully recover once it emerges from the bear market.

“How do my financial goals help me cope with market volatility?”

When we reviewed financial objectives, we saw that it was useful to break goals down by time and priority. Then match investment patterns to the objectives.

Investing for retirement in 40 years is very different than saving for a house in 3 years. The 40 year time frame allows for increased investment risk (volatility) in exchange for higher expected returns over time. Short term goals cannot withstand being on the wrong side of market corrections. Instead, investors sacrifice potential return in exchange for safety of capital and liquidity. That is the risk-return relationship.

By matching investments to objectives you remove some of the volatility worries on near term priorities.

“Will my target asset allocation help address volatility concerns?”

An investor’s target asset allocation directly reflects one’s Investor Profile. Which includes financial objectives, constraints, time horizon, financial situation, and risk tolerance.

A proper asset allocation will help set up investments and classes to meet your goals.

As we saw above, matching investment risk to a specific objective will assist in managing volatility. If you invest in more stable investments for a 1 year goal, you are at less risk of market disruption than if invested in riskier, more volatile, assets.

If you invest in higher risk assets for a 35 year retirement goal, you will be more prone to market bull and bear fluctuations. But that long time frame allows you to ride out the ups and downs. As you approach retirement, your time horizon moves from long to medium and then short term. As time lessens, you should slowly shift your assets into lower risk products.

“Portfolio diversification manages investment risk. What about with overall volatility?”

Another aspect of the target asset allocation is diversification. Combining assets with low or negative correlations to manage portfolio risk.

For example, Portfolio Visualizer shows the correlation coefficient between the S&P 500 and US 1-3 Year Treasury Bonds at -0.40 (based on monthly returns from time 01/01/2008 – 06/30/2021).

If you recall our asset correlation discussion, assets with negative correlations tend to move in opposite directions. If the S&P 500 increases, we would expect decreases in the US shorter-term bond market. If the S&P 500 falls or enters a bear market, we would now experience gains on the bond portfolio.

How you diversify your target asset allocation helps cope with market volatility in any one asset class.

“Is combining Dollar Cost Averaging (DCA) with Buy and Hold useful?”

At $10 per unit, you can purchase 100 units. If the market rises (upside volatility) to $20, you will only be able to buy 50 units. If the market corrects or enters a bear market and prices fall to $5, your $1000 now gets you 200 units.

History shows that over longer time periods, assets appreciate in value. By combining DCA with Buy and Hold you are actually purchasing additional units at a price discount. For younger investors with long time horizons, corrections may be seen as Black Friday Sales events. Why pay $20 when you can pay $5 for the same asset?

“Why is cost minimization so important? Especially in bear markets.”

Costs are important whether the markets are up or down. Cost minimization is key to investing success.

So why is it “especially” important in bear markets?

Probably more of a psychological and behavioural finance issue.

You own an US equity fund. When it returns 18%, you may not be too concerned paying 1.5% in Management Expense Ratio (MER). But what if the fund returns 1.5% or -2.0%? That MER has wiped out your return or almost doubled your loss for the year. Same MER. But in a flat or bear market, investors “feel” the costs to a higher degree.

And no, you do not see fund managers refunding fees to investors in bad times.

There are valid criticisms when using a Buy and Hold investment strategy. Potentially sub-optimal returns. No bear-market protection. Possible need for a very long time horizon. A review of these legitimate concerns when using Buy and Hold.

“If Buy and Hold does not allow for maximum returns, why use it?”

An argument in favor of active management. If you are agile and a strong asset selector, you can improve upon performance over a hold approach.

However, as we have seen over and over again, active management tends not to outperform a passive approach. On a consistent basis over longer periods. We covered this in “Episode 36: Passive versus Active Management Data”.

“Buy and Hold does not provide down-market protection. Should I market time?”

The same issue holds with down-market protection.

Yes, in a Buy and Hold you sit tight through down markets. Maybe you experience unrealized losses. Some fairly significant. Also, there is the stress of watching your net worth fall, while you do nothing.

But, as we saw with active management, getting the market timing right is not easy. If it was, the professional investors would jump out and back in after the fall on a consistent basis. And easily beat their benchmark returns. They do not.

Part of the problem is identifying when a market will move. As we discussed in “Episode 38: Investor Behaviour”, simply missing out on the best 5 or 30 out of 13,870 market days can decrease portfolio growth by 35% and 81% respectively.

It is usually better to remain invested and not miss out, than get the timing wrong.

“What if I am not immortal and cannot wait forever for Buy and Hold to succeed?”

In the long run, assets appreciate. In the shorter term, there may be market volatility. Assets do not steadily climb in value.

The question is, how long must you wait to see that growth. Especially when enduring a substantial and/or lengthy correction. That is a risk.

This comes back to diversification and risk-return relationship. Then matching investments to specific financial goals.

If you have a 40 year time horizon until retirement, you can take on added investment risk (i.e., volatility). Over time, the price swings will even out and you should receive higher returns for the extra risk.

If you have 2 years to save for a home down-payment, you cannot take on that extra volatility. You do not have the time frame to allow for price swings (in both directions) to average out. Instead, you sacrifice return for certainty and safety.

By matching investment risk-return profiles to the time horizon of a specific objective, you can eliminate some of the concerns from market volatility and bear markets.

We saw this in the graph from “Why Use Lump Sum Investing?”. Over time, assets appreciate. Over time, the riskier assets appreciate more than the less risky asset classes. But throughout the time frame, in short to medium terms, there is greater price volatility in the higher risk classes.

We also saw this in “Episode 5: Standard Deviation”. Where we view volatility from a quantitative perspective. The higher the investment risk, the more likely the actual outcome will differ from the expected result. What you choose to invest in will dictate how volatile the asset will be.

There are a few criticisms of investing using a Buy and Hold strategy. Some are legitimate. Some, much less so. With claims that Buy and Hold is too easy, too unsophisticated, too stressful, and is obsolete in today’s investment world. A look at these perceived disadvantages of Buy and Hold investing.

“Buy and Hold is an easy investment strategy. Is it too easy for investors?”

Yes, Buy and Hold is quite easy. But ease does not mean it is ineffective.

The bigger issue is that the ease of this approach can create lazy investors. That is a legitimate concern.

Investors must remember that it is Buy and Hold, not Buy and Forget. Investors still must monitor their portfolios and holdings. As conditions change, maybe investments need to be fine-tuned. Back to the target asset allocation. When the product is no longer best in class. When your Investor Profile changes and you need to amend the target asset allocation.

“Investing success requires sophisticated traded systems. Can Buy and Hold work in a complex world?”

Yes, there are many complex trading strategies available. They require expertise and time. Often with higher costs to implement as complex strategies tend to be quite active.

The reality is that sophisticated approaches usually do not outperform a simple strategy. Read investing advice from people like Warren Buffett or John Bogle. A simple approach is often the best one.

“You stated Buy and Hold helps manage emotions. But I read it is actually stressful. Which is correct?”

For some investors though, that discipline can be a two-edged sword. When the markets are falling and the experts are predicting more doom and gloom, it can be hard to stay on track and hold onto your investments.

And if you are invested in non-diversified assets, it can be stressful. But in our overall investment approach, you should combine Buy and Hold with Dollar Cost Averaging as you build a portfolio of well-diversified, low-cost, index funds.

Under this approach, in down markets you will be buying additional shares at discounts and smoothing your cost base. As the assets are well-diversified, you do not need to worry about owning the next Enron or Kodak. That stock specific risk is not an issue. Less of a stressor adding quality assets at price discounts.

You understand investing principles. The risk-return relationship. How actively trading and trying to time market volatility tends not to be successful. That in the long-term, assets increase in value, even if there are corrections and dips along the way. In buying the entire market, you understand you will be fine over time in holding your assets.

The entire investment approach and your new knowledge will serve to alleviate the stress in rocky times.

“I read Buy and Hold had its moments. But in today’s computerized world, it is obsolete. Yes or no?”

Yes, there are better tools and access to information now. Many investors use technical analysis and software programs to actively trade and take advantage of short-term price inefficiencies. Investors have better access to corporate information and use fast trading platforms. A short-term trading approach is much easier and effective than 10-20 years ago.

But does that mean Buy and Hold is obsolete? Does it have to be an either/or prospect?

I would say no. As I have discussed previously, I do not think that technical analysis and very active trading does bring investment success for most investors. Especially those reading this post. If you want to develop expertise in technical analysis and become a full-time trader, that is one thing. If you are a doctor, teacher, engineer, lawyer, you work a full-day in your own area of expertise. Can you compete part-time against these investing professionals?

“How do my financial goals help me cope with market volatility?”

“How do my financial goals help me cope with market volatility?”