A legitimate concern when using a Buy and Hold investment strategy is managing market volatility. How do investors use complementary investment strategies and tactics to reduce risk in bear-markets and short-term fluctuations.

“What exactly is a ‘bear’ market? How does it differ from a ‘bull’ market?”

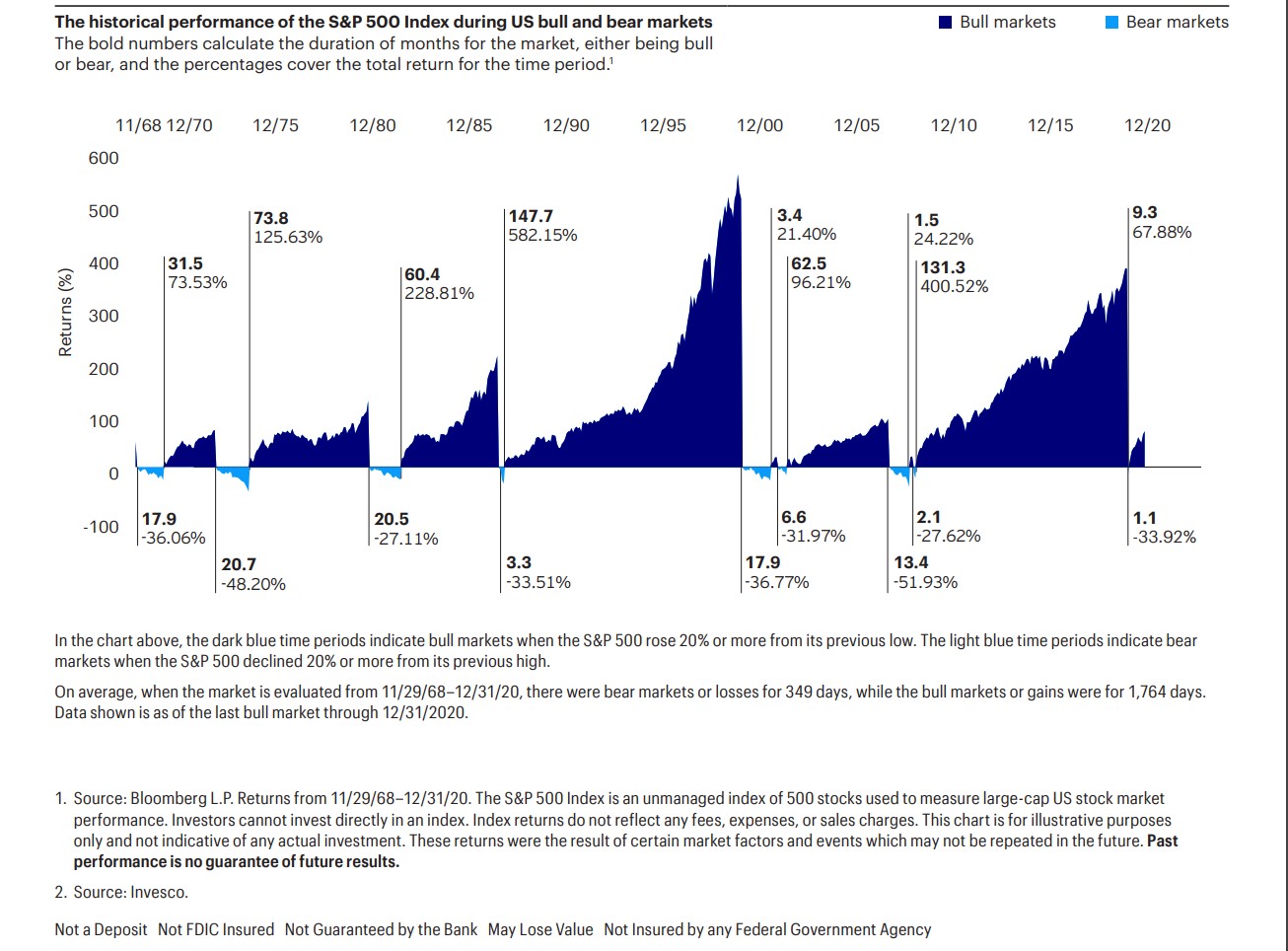

A bear market is a prolonged period of falling prices. Usually, 20% from its previous high.

A bull market is a prolonged period of rising prices. Usually, rising at least 20% from its previous low.

“What is an average time period for bull and bear markets?”

Per Invesco, from 1968 to the end of 2020, the average bull market has averaged 1764 days in length (4.8 years). Once a bull gets underway, it tends to stay for an extended period.

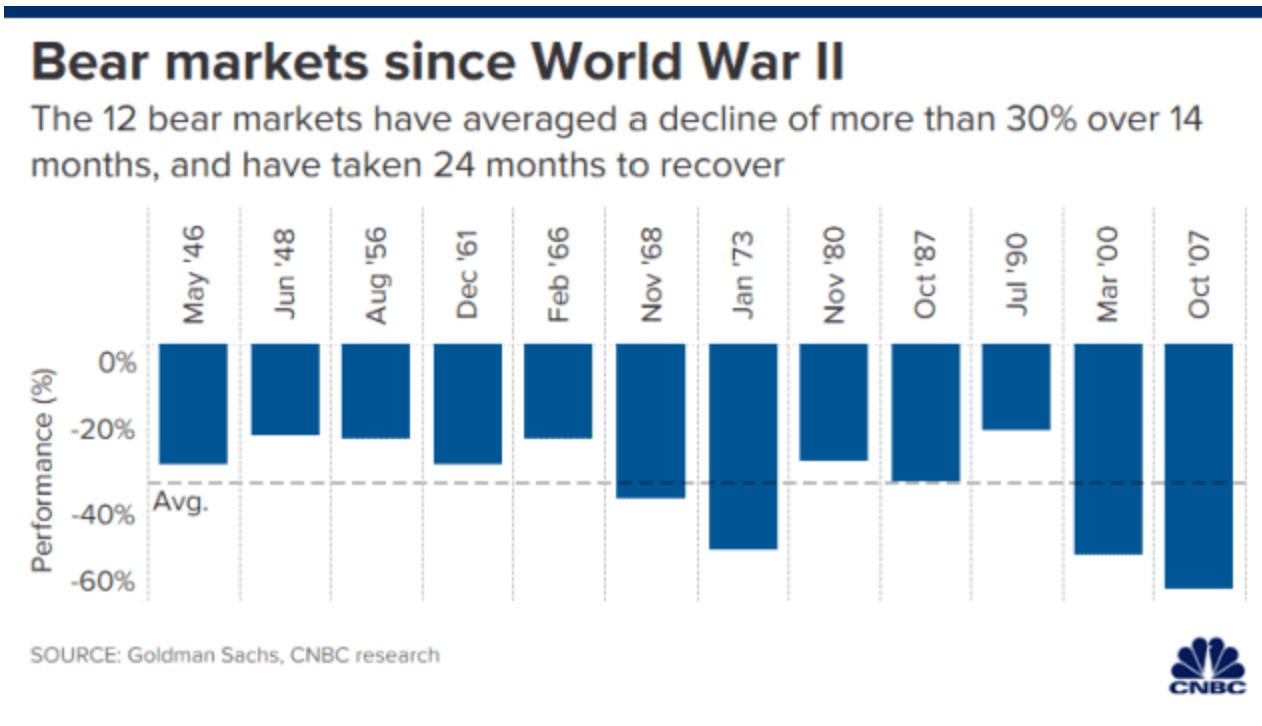

During that same period, there have only been about 7 truly, sustained bear markets that were over 90 days in length. The average length of a bear market has been 349 days. Much shorter in duration than the bull runs.

However, one must factor in the recovery time as well. If you purchased at $100 and it fell to $70, you want to assess how low it took to get back to $100. Not just when the bear market ended and prices began to increase.

Per Goldman Sachs, it has taken the S&P 500 about 24 months to fully recover once it emerges from the bear market.

“How do my financial goals help me cope with market volatility?”

When we reviewed financial objectives, we saw that it was useful to break goals down by time and priority. Then match investment patterns to the objectives.

Investing for retirement in 40 years is very different than saving for a house in 3 years. The 40 year time frame allows for increased investment risk (volatility) in exchange for higher expected returns over time. Short term goals cannot withstand being on the wrong side of market corrections. Instead, investors sacrifice potential return in exchange for safety of capital and liquidity. That is the risk-return relationship.

By matching investments to objectives you remove some of the volatility worries on near term priorities.

“Will my target asset allocation help address volatility concerns?”

An investor’s target asset allocation directly reflects one’s Investor Profile. Which includes financial objectives, constraints, time horizon, financial situation, and risk tolerance.

A proper asset allocation will help set up investments and classes to meet your goals.

As we saw above, matching investment risk to a specific objective will assist in managing volatility. If you invest in more stable investments for a 1 year goal, you are at less risk of market disruption than if invested in riskier, more volatile, assets.

If you invest in higher risk assets for a 35 year retirement goal, you will be more prone to market bull and bear fluctuations. But that long time frame allows you to ride out the ups and downs. As you approach retirement, your time horizon moves from long to medium and then short term. As time lessens, you should slowly shift your assets into lower risk products.

“Portfolio diversification manages investment risk. What about with overall volatility?”

Another aspect of the target asset allocation is diversification. Combining assets with low or negative correlations to manage portfolio risk.

For example, Portfolio Visualizer shows the correlation coefficient between the S&P 500 and US 1-3 Year Treasury Bonds at -0.40 (based on monthly returns from time 01/01/2008 – 06/30/2021).

If you recall our asset correlation discussion, assets with negative correlations tend to move in opposite directions. If the S&P 500 increases, we would expect decreases in the US shorter-term bond market. If the S&P 500 falls or enters a bear market, we would now experience gains on the bond portfolio.

How you diversify your target asset allocation helps cope with market volatility in any one asset class.

“Is combining Dollar Cost Averaging (DCA) with Buy and Hold useful?”

At $10 per unit, you can purchase 100 units. If the market rises (upside volatility) to $20, you will only be able to buy 50 units. If the market corrects or enters a bear market and prices fall to $5, your $1000 now gets you 200 units.

History shows that over longer time periods, assets appreciate in value. By combining DCA with Buy and Hold you are actually purchasing additional units at a price discount. For younger investors with long time horizons, corrections may be seen as Black Friday Sales events. Why pay $20 when you can pay $5 for the same asset?

“Why is cost minimization so important? Especially in bear markets.”

Costs are important whether the markets are up or down. Cost minimization is key to investing success.

So why is it “especially” important in bear markets?

Probably more of a psychological and behavioural finance issue.

You own an US equity fund. When it returns 18%, you may not be too concerned paying 1.5% in Management Expense Ratio (MER). But what if the fund returns 1.5% or -2.0%? That MER has wiped out your return or almost doubled your loss for the year. Same MER. But in a flat or bear market, investors “feel” the costs to a higher degree.

And no, you do not see fund managers refunding fees to investors in bad times.

There are valid criticisms when using a Buy and Hold investment strategy. Potentially sub-optimal returns. No bear-market protection. Possible need for a very long time horizon. A review of these legitimate concerns when using Buy and Hold.

“If Buy and Hold does not allow for maximum returns, why use it?”

An argument in favor of active management. If you are agile and a strong asset selector, you can improve upon performance over a hold approach.

However, as we have seen over and over again, active management tends not to outperform a passive approach. On a consistent basis over longer periods. We covered this in “Episode 36: Passive versus Active Management Data”.

“Buy and Hold does not provide down-market protection. Should I market time?”

The same issue holds with down-market protection.

Yes, in a Buy and Hold you sit tight through down markets. Maybe you experience unrealized losses. Some fairly significant. Also, there is the stress of watching your net worth fall, while you do nothing.

But, as we saw with active management, getting the market timing right is not easy. If it was, the professional investors would jump out and back in after the fall on a consistent basis. And easily beat their benchmark returns. They do not.

Part of the problem is identifying when a market will move. As we discussed in “Episode 38: Investor Behaviour”, simply missing out on the best 5 or 30 out of 13,870 market days can decrease portfolio growth by 35% and 81% respectively.

It is usually better to remain invested and not miss out, than get the timing wrong.

“What if I am not immortal and cannot wait forever for Buy and Hold to succeed?”

In the long run, assets appreciate. In the shorter term, there may be market volatility. Assets do not steadily climb in value.

The question is, how long must you wait to see that growth. Especially when enduring a substantial and/or lengthy correction. That is a risk.

This comes back to diversification and risk-return relationship. Then matching investments to specific financial goals.

If you have a 40 year time horizon until retirement, you can take on added investment risk (i.e., volatility). Over time, the price swings will even out and you should receive higher returns for the extra risk.

If you have 2 years to save for a home down-payment, you cannot take on that extra volatility. You do not have the time frame to allow for price swings (in both directions) to average out. Instead, you sacrifice return for certainty and safety.

By matching investment risk-return profiles to the time horizon of a specific objective, you can eliminate some of the concerns from market volatility and bear markets.

We saw this in the graph from “Why Use Lump Sum Investing?”. Over time, assets appreciate. Over time, the riskier assets appreciate more than the less risky asset classes. But throughout the time frame, in short to medium terms, there is greater price volatility in the higher risk classes.

We also saw this in “Episode 5: Standard Deviation”. Where we view volatility from a quantitative perspective. The higher the investment risk, the more likely the actual outcome will differ from the expected result. What you choose to invest in will dictate how volatile the asset will be.

There are a few criticisms of investing using a Buy and Hold strategy. Some are legitimate. Some, much less so. With claims that Buy and Hold is too easy, too unsophisticated, too stressful, and is obsolete in today’s investment world. A look at these perceived disadvantages of Buy and Hold investing.

“Buy and Hold is an easy investment strategy. Is it too easy for investors?”

Yes, Buy and Hold is quite easy. But ease does not mean it is ineffective.

The bigger issue is that the ease of this approach can create lazy investors. That is a legitimate concern.

Investors must remember that it is Buy and Hold, not Buy and Forget. Investors still must monitor their portfolios and holdings. As conditions change, maybe investments need to be fine-tuned. Back to the target asset allocation. When the product is no longer best in class. When your Investor Profile changes and you need to amend the target asset allocation.

“Investing success requires sophisticated traded systems. Can Buy and Hold work in a complex world?”

Yes, there are many complex trading strategies available. They require expertise and time. Often with higher costs to implement as complex strategies tend to be quite active.

The reality is that sophisticated approaches usually do not outperform a simple strategy. Read investing advice from people like Warren Buffett or John Bogle. A simple approach is often the best one.

“You stated Buy and Hold helps manage emotions. But I read it is actually stressful. Which is correct?”

For some investors though, that discipline can be a two-edged sword. When the markets are falling and the experts are predicting more doom and gloom, it can be hard to stay on track and hold onto your investments.

And if you are invested in non-diversified assets, it can be stressful. But in our overall investment approach, you should combine Buy and Hold with Dollar Cost Averaging as you build a portfolio of well-diversified, low-cost, index funds.

Under this approach, in down markets you will be buying additional shares at discounts and smoothing your cost base. As the assets are well-diversified, you do not need to worry about owning the next Enron or Kodak. That stock specific risk is not an issue. Less of a stressor adding quality assets at price discounts.

You understand investing principles. The risk-return relationship. How actively trading and trying to time market volatility tends not to be successful. That in the long-term, assets increase in value, even if there are corrections and dips along the way. In buying the entire market, you understand you will be fine over time in holding your assets.

The entire investment approach and your new knowledge will serve to alleviate the stress in rocky times.

“I read Buy and Hold had its moments. But in today’s computerized world, it is obsolete. Yes or no?”

Yes, there are better tools and access to information now. Many investors use technical analysis and software programs to actively trade and take advantage of short-term price inefficiencies. Investors have better access to corporate information and use fast trading platforms. A short-term trading approach is much easier and effective than 10-20 years ago.

But does that mean Buy and Hold is obsolete? Does it have to be an either/or prospect?

I would say no. As I have discussed previously, I do not think that technical analysis and very active trading does bring investment success for most investors. Especially those reading this post. If you want to develop expertise in technical analysis and become a full-time trader, that is one thing. If you are a doctor, teacher, engineer, lawyer, you work a full-day in your own area of expertise. Can you compete part-time against these investing professionals?

What are the potential advantages in using a Buy and Hold investing strategy? For investors: ease of use; consistency with investment theory; promotes good investing habits. Buy and Hold also works well when combined with Dollar Cost Averaging (DCA) and a passive investment management approach. Strategies that I also recommend.

“Why is Buy and Hold an ‘easy’ investment strategy?”

Buy and Hold is very easy. For investors to understand. To implement. And to maintain.

You identify an investment. Buy it. Then hold until you reach your financial objective’s time horizon.

Sometimes, Buy and Hold may be too easy. As we will discuss in future episodes.

“How is Buy and Hold consistent with investment theory?”

In prior episodes, we have seen that assets appreciate over time. If you buy and hold an investment, over the long term it will grow in value. The greater the investment risk of the asset, the greater the growth.

“How will Buy and Hold improve my investing habits?”

Much like we saw with DCA, Buy and Hold will improve investing consistency and discipline.

Without worrying about when to buy and sell an asset, Buy and Hold takes emotions out of the equation. Making the investment process more consistent and disciplined.

“Why does Buy and Hold work well with passive investing?”

Buy an asset. Then hold it through the time horizon. With no trading, costs remain low.

Perfect for passive investors. Perhaps, too perfect (this is what is known as foreshadowing!).

“And DCA?”

Again, identify the “best in class” asset. Then, slowly add to that position over time using DCA. When you reach the financial objective’s time horizon, divest.

A Buy and Hold strategy will have lower transaction costs than a more active approach.

It may also trigger fewer taxable events. If you hold your investments in a taxable investment account, every time you sell, you may incur (hopefully) a capital gains tax. The sooner you have to pay tax, the less cash you have available to reinvest and grow.

Under Buy and Hold, you will have fewer dispositions. Resulting in fewer taxable events. The longer you can let your wealth compound in your own accounts, and not the tax-man’s, the better.

As well, there is likely an opportunity cost that comes from actively trading. In “Episode 38: Investor Behaviour”, we saw the portfolio growth impact from minimal misses in timing the markets.

Between January 1, 1980 and December 31, 2018, had you missed out on just the 5 best market days of the S&P 500, your portfolio would have a 35% decrease versus being fully in the market the entire time. Missing the best 30 days out of 13,870? Your portfolio would be worth 81% less.

A Buy and Hold strategy might have been better than jumping in and out of the S&P 500.

Another investing debate involves ongoing portfolio maintenance. Should you buy an asset and then hold it “forever”? Or is it wiser to more actively trade investment holdings? At the extreme, high frequency (a.k.a. day) trading. Or somewhere in between day trading and never selling. An introduction to the “Buy and Hold versus Active Trading” debate.

As the name suggests, you identify an investment. You purchase it. Then hold it throughout the entire time horizon. That may be 3 year time horizon in amassing a down payment on a new home. It may be 40 years for your retirement.

“Is Active Management the same as Active Trading?”

Yes and no.

Active management is the investment strategy. Where asset managers decide they will identify good (and bad) investments and market timing opportunities. Then trade accordingly. Many professional money managers take a longer term approach to their holdings. Although, in this context, longer term may be 2-3 years. Not 40. Identify strong assets, buy, then hold until the target price is reached or circumstances change.

Active trading is more the investment tactic to achieve one’s strategy. Though, not always. Depends on the nature of the investor and strategy.

Strategy is the overall, long-term, planned approach. Tactics are the short term processes used to implement the strategy.

For me, active management typically means I identify an investment strategy. Perhaps outperforming the US large cap equity market. I comb through the S&P 500 index and identify the best stocks. Invest in them and ignore the rest. I also over or underweight sectors or stocks based on overall market conditions. The timing aspect. Through these I should beat my benchmark index.

Active trading is the implementation of the strategy. Maybe I determine only 50 stocks are worth owning. I buy them and trade as they reach the target price, a better holding is determined, or a market shift is anticipated. The frequency of the trading is a reflection of meeting my strategic objectives. Not just trading for the sake of trading.

Yes, the same thing. But usually a different meaning when discussed.

And yes, some investors do trade for the sake of trading.

“What is High Frequency trading?”

Also known as day trading, these investors can be very active. Possibly buying and selling the same holding multiple times in a single trading day.

Day traders normally use quantified technical analysis to identify price inefficiencies in assets. Or pricing trends. They may buy and sell in rapid fashion to take advantage of these small variances.

In this case, the high frequency trading is its own investment strategy.

“Which approach do most investors utilize?”

Most investors are not day traders. That area is more of a niche that requires special skills, experience, and time commitment. As well, these investors often require significant capital to invest.

That said, most investors are not hold forever, either.

Most investors buy when they believe the markets are down or a specific investment is trading at a discount to fair value. These same investors may divest when they believe the market or asset is over-valued. Perhaps they sell and move on to other investments. Or they wait for a downswing and then repurchase the same holding.

Market timing, type of asset, and emotional considerations all play a role in trading frequency. My general belief is that the average investor trades too frequently and that hurts performance and portfolio growth.

“What part of the spectrum do you think is the sweet spot?”

How active one should be as an investor tends to be more a function of the asset itself.

If you are invested in a well-diversified, low-cost, index fund, that is an investment that can be held forever without issue.

If you are invested in non-diversified or highly volatile assets, you may need to monitor more closely. And fine tune periodically.

I tend to prefer well-diversified index funds for investors. So, I am more on the hold forever side. However, “buy and hold” does not mean “buy and forget”. There must be mechanisms in place to ensure the quality assets you own remain quality assets in the future.

A quick introduction to Buy & Hold. We will get into more nuance over the next few episodes on the relative advantages and disadvantages of this approach.

“How do my financial goals help me cope with market volatility?”

“How do my financial goals help me cope with market volatility?”